Taking out a loan can be a strategic move toward achieving your financial goals, but it’s important to navigate the process carefully to avoid potential setbacks. For Canadians exploring personal loans, payday loans, or alternatives like lines of credit, understanding common pitfalls is essential.

Some common mistakes include overborrowing, neglecting to read the fine print, relying on loans for everyday expenses, not considering other options, and making late or missed payments. Being aware of these potential errors and knowing how to avoid them can pave the way for a more stable and successful financial journey.

Navigating the Canadian Loan Landscape

The world of loans becomes easier to navigate when you know what types of loans are available. In Canada, there are a variety of loan and money-borrowing options. 3 of the most common include personal loans, payday loans, and lines of credit.

Personal Loans

Personal loans are versatile financial tools that can be used for a variety of purposes, from consolidating debt to making a large purchase. They can be unsecured, meaning you don’t need to provide collateral.

Secured term loans are tied to something you own, using the asset as collateral in the event that you cannot pay the loan. Providing collateral typically allows you to borrow larger amounts.

Regardless of the personal loan, interest rates can vary depending on your credit score and the lender’s terms.

Eligibility for personal loans generally depends on your creditworthiness, income, and employment status. It’s important to understand these criteria before applying, as they directly influence the loan amount and interest rate you may qualify for.

Payday Loans

Payday loans are short-term, high-interest loans designed to tide you over until your next paycheck. While they may seem like a quick fix for financial troubles, they come with significant risks. The ease of access and minimal eligibility requirements often lead people into a cycle of debt that’s hard to escape.

These loans can be costly due to their high interest rates, often leaving borrowers paying significantly more than the original loan amount. It’s crucial to consider this before opting for a payday loan.

Lines of Credit

A line of credit offers a fixed credit limit that you can borrow against as needed, much like a credit card. This flexibility makes it an attractive option for those who require ongoing access to funds.

Lines of credit can be secured or unsecured, with interest rates typically lower than credit cards but higher than personal loans. Eligibility for a line of credit often requires a good credit score and a stable income, so borrowers should be aware of their financial standing before applying.

Avoiding Common Loan Pitfalls

With a clear understanding of the types of loans available, you can better avoid common pitfalls. Going into your loan journey, be aware of the risks of overborrowing, entering loan agreements without a full understanding, and not being prepared to make payments.

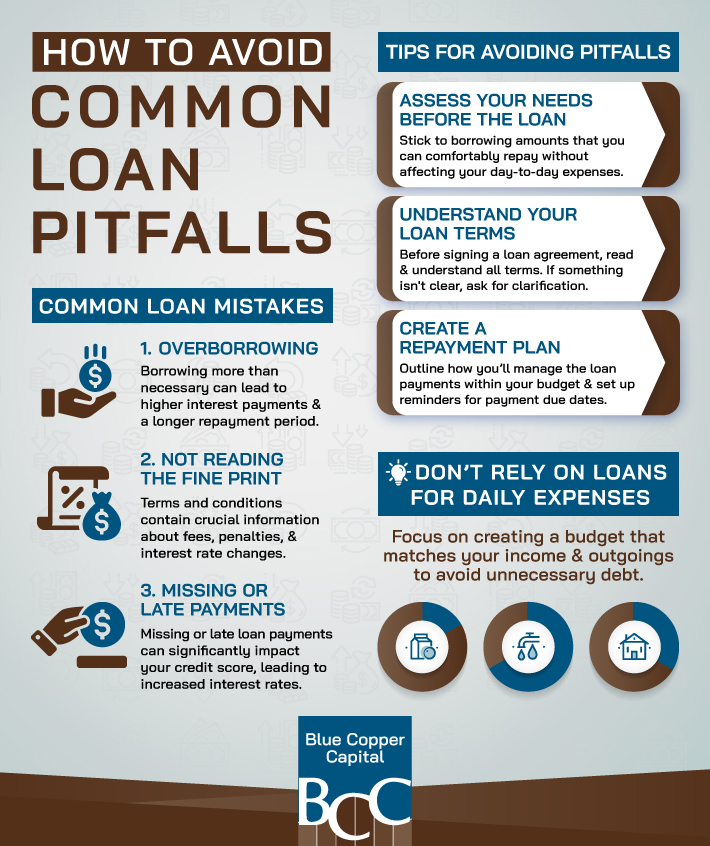

- Overborrowing

Overborrowing is a trap many fall into, often without realizing it. It’s easy to be tempted by a larger loan amount than you actually need, especially when lenders are willing to offer it. However, borrowing more than necessary can lead to higher interest payments and a longer repayment period, straining your finances.

To avoid overborrowing, assess your actual needs before applying for a loan. Stick to borrowing amounts that you can comfortably repay without affecting your day-to-day expenses.

- Ignoring the Fine Print

Loan agreements can be dense and full of jargon, leading many borrowers to skim over important details. However, ignoring the fine print can have serious consequences. Terms and conditions often contain crucial information about fees, penalties, and interest rate changes.

Before signing any loan agreement, take the time to read and understand all terms. If something isn’t clear, ask the lender for clarification. It’s better to spend a little extra time on the details than to face unexpected costs later.

- Relying on Loans for Daily Expenses

Using loans to cover daily expenses can quickly lead to a cycle of debt. It might offer temporary relief, but it often results in long-term financial strain. When loans are used for everyday costs, borrowers may find themselves consistently falling behind on payments.

Instead of relying on loans for daily expenses, focus on creating a budget that matches your income and outgoings. This can help you avoid unnecessary debt and foster healthier financial habits.

- Not Considering Alternatives

When in need of funds, it’s easy to focus solely on loans as the solution. However, there are alternative financial options that might be more suitable. These include using savings, adjusting your budget, or even seeking financial advice for better money management strategies.

Considering all available options before taking out a loan can prevent unnecessary debt and lead to a more secure financial future.

- Missing or Late Payments

Missing or making late loan payments can significantly impact your credit score, leading to increased interest rates and difficulties obtaining credit in the future. Consistently falling behind on payments can also put you at risk of default, which can have long-lasting repercussions.

To avoid these issues, set up reminders for payment due dates or automate your payments if possible. Keeping up with timely payments helps maintain your credit score and keeps loan-related stress at bay.

Tips for Responsible Borrowing

Borrowing responsibly involves understanding your financial situation and making informed decisions. Here are some tips to ensure you borrow wisely.

Understand Your Financial Needs & Capacity

Before applying for any loan, thoroughly evaluate your financial needs and capacity. Determine how much you need and how much you can afford to repay each month. This understanding will guide your borrowing decisions and help you avoid taking on more than you can handle.

Consider using financial planning tools or consulting a financial advisor to gain a clearer picture of your financial health and borrowing capabilities.

Research & Compare Different Lenders

Not all lenders are the same. Interest rates, loan terms, and customer service can vary significantly from one lender to another.

Research and compare different options to find a lender that offers the best fit for your needs. Look for lenders who are transparent about their terms and have a reputation for ethical practices.

Create a Repayment Plan

Having a repayment plan in place before taking out a loan can make a significant difference. This plan should outline how you’ll manage the loan payments within your budget, helping you avoid falling behind on payments.

Consider factors like the loan term, interest rate, and any potential changes in your financial situation when creating your repayment strategy.

Build an Emergency Fund

An emergency fund provides a financial safety net, reducing your reliance on loans in times of need. By setting aside a small amount of money each month, you can gradually build an emergency fund that covers unexpected expenses like medical bills or car repairs.

Having an emergency fund can prevent you from needing to take out additional loans for unforeseen costs, helping you maintain financial stability.

Moving Forward with Confidence

Navigating the world of loans may seem daunting, but with the right knowledge and approach, it can be manageable. By being aware of common pitfalls and practicing responsible borrowing, you can make informed financial decisions that support your goals instead of hindering them.

Remember, borrowing is all about how you manage it. For personalized advice and ethical lending options, reach out to our team at Blue Copper Capital. We can help you find the right financial solutions and support you on your borrowing journey.