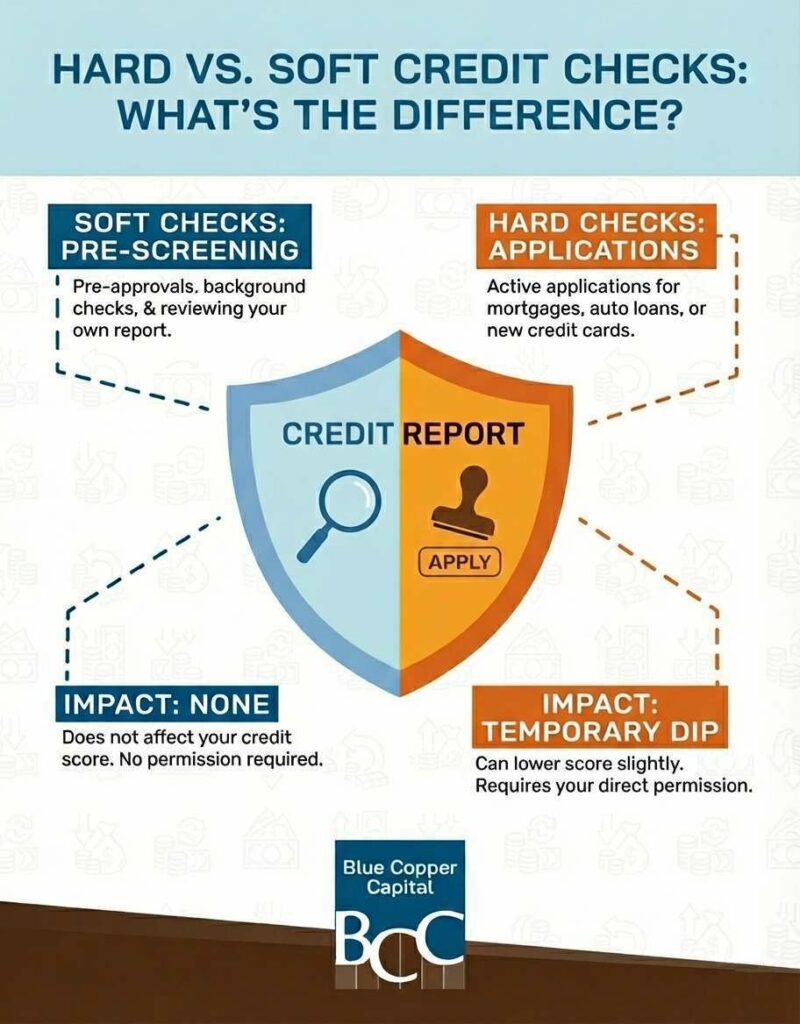

Hard vs. Soft Credit Checks: What’s the Difference?

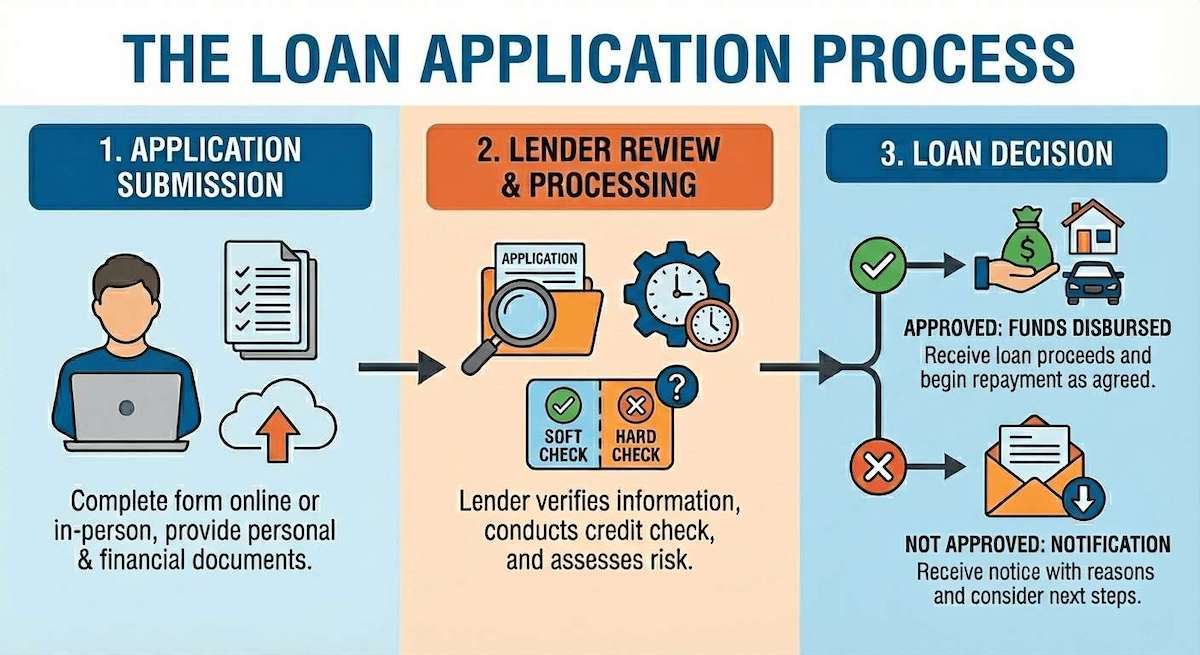

When you apply for personal or business loans, lenders need to check your credit. You might wonder why some credit checks seem to hurt your credit score while others don’t affect it at all.

The main difference comes down to impact: soft credit checks don’t affect your credit score and happen without your direct permission, while hard credit checks can lower your score temporarily and require your approval for specific loan or credit applications.

Understanding this difference is especially important when you’re working with a licensed lender like Blue Copper Capital, who prioritizes transparent lending and explains how credit inquiries affect your score.

What Are Credit Checks & Why Do Lenders Use Them?

How Credit Checks Work

Credit checks happen when someone requests information from your credit report. Credit bureaus like Equifax and TransUnion keep detailed records of your borrowing history, payment patterns, and current debts.

When a lender, employer, or other organization wants to see this information, they contact the credit bureau. The bureau then provides a snapshot of your financial behaviour based on your credit history.

Why Lenders Review Your Credit History

Licensed lenders in Alberta and BC use credit checks to understand how you’ve handled money in the past. Your credit history helps them decide whether to approve your loan application and what interest rate to offer.

For payday loans or short-term loans, lenders want to see if you typically pay bills on time. They also look at how much debt you already carry compared to your available credit.

What Information Shows Up on Credit Reports

Your credit report includes your payment history, current account balances, and types of credit accounts you have open. It also shows any missed payments, collections, or bankruptcies from recent years.

The report lists every time someone has checked your credit, along with basic personal information like your current and previous addresses. This data helps create your overall credit score.

Soft Credit Checks Explained

What Happens During a Soft Credit Check

A soft credit check gives a basic overview of your credit without affecting your score. These checks often happen in the background when companies want to pre-screen you for offers or verify your identity.

You won’t always know when soft checks occur because they don’t require your specific permission for each instance. However, you can see them listed on your credit report.

Common Examples of Soft Inquiries

- Pre-approval offers from credit card companies: Companies check basic credit information to see if you qualify before sending you promotions.

- Checking your own credit report: Reviewing your own credit through Equifax, TransUnion, or a credit monitoring app is always a soft check.

- Insurance quote applications: Insurance providers sometimes run soft checks to help determine your eligibility or premium level.

- Background checks by employers: While not very common in Canada, some employers may run a soft credit check for roles involving financial responsibilities or security screening. These checks don’t affect your credit score.

How Soft Checks Affect Your Credit Score

Soft credit checks have zero impact on your credit score. You can have dozens of soft inquiries without any negative effects on your ability to get approved for loans.

This means you can safely check your own credit report regularly or get insurance quotes without worrying about damaging your credit standing.

Hard Credit Checks Explained

What Happens During a Hard Credit Check

Hard credit checks provide detailed information about your credit history when you actively apply for new credit. These inquiries require your permission and indicate you’re seriously considering taking on new debt.

Lenders use hard checks when you submit applications for personal loans, business loans, car loans, or lines of credit. The detailed report helps them make final approval decisions.

When Hard Inquiries Occur

- Mortgage applications: Lenders run a full credit check to assess risk before approving a home loan.

- Auto loan applications: Car financing always requires a hard inquiry to confirm your payment history and current debts.

- Credit card applications: Applying for a new credit card triggers a hard check because you’re asking for a new line of credit.

- Personal and business loan applications: Whether you apply for personal loans, short-term loans, or business financing, lenders review your full credit file to make approval decisions.

How Hard Checks Impact Your Credit Score

Each hard inquiry can lower your credit score by a few points, typically between 2-10 points. The impact usually fades within a few months, and the inquiry disappears from your report after two years. If you’re approved, and payment history, loan history, and utilization are reporting positively, this can quickly negate the impact from a hard check.

Multiple hard checks in a short period can signal financial stress to lenders, especially if you’re applying for different types of credit simultaneously.

For your overall credit health, there’s no need to be preoccupied with hard credit checks as long as you’re applying for credit responsibly. Making sure to pay on time, having different types of credit, paying down your debt, having longer histories with credit cards and lines of credit will all have greater influence.

Key Differences Between Hard & Soft Credit Checks

Impact on Your Credit Score

The biggest difference lies in how these checks affect your credit score. Soft checks have no consequences, while hard checks can temporarily reduce your score.

If you’re shopping for flexible loan options, knowing this difference helps you understand when your credit might be affected during the application process.

Who Can See These Inquiries

Other lenders can see hard inquiries on your credit report, which might influence their lending decisions. Soft inquiries typically only show up when you view your own credit report.

This visibility means multiple recent hard checks might make it harder to get approved for additional credit in the short term. Understanding why credit scores matter helps you make informed borrowing decisions.

How Long They Stay on Your Credit Report

Both types of inquiries remain on your credit report for two years. However, hard inquiries only affect your credit score calculation for the first 12 months.

After that first year, hard checks become more like soft checks, visible on your report but not impacting your score.

Permission Requirements

Hard credit checks always require your explicit permission, usually through a signed loan or credit application. Lenders must clearly inform you that a hard inquiry will occur before pulling your report.

Soft credit checks, on the other hand, can happen when you’ve given general consent, such as when you already have an existing account and request a pre-approval. These checks are used for verification or promotional purposes and don’t affect your credit score.

Making Credit Checks Easier to Understand

Understanding how credit checks work helps you make informed decisions about your financial future. At Blue Copper Capital, we believe in transparent lending and take the time to walk you through the loan process — including how hard and soft inquiries may affect your credit in your specific situation.

Whether you’re looking for personal loans in Calgary, business loans in Vancouver, or other financing options in Alberta or BC, our licensed team is here to help you explore your options while protecting your credit health.