When it comes to managing finances, a line of credit offers flexibility that can be hard to beat. Whether it’s a home equity line of credit (HELOC) or a personal line of credit, understanding how interest is calculated is key to making smart financial decisions.

Interest on a line of credit is typically calculated based on the amount you borrow, not the total credit limit. Most lines of credit use a variable interest rate, which means the rate can fluctuate over time.

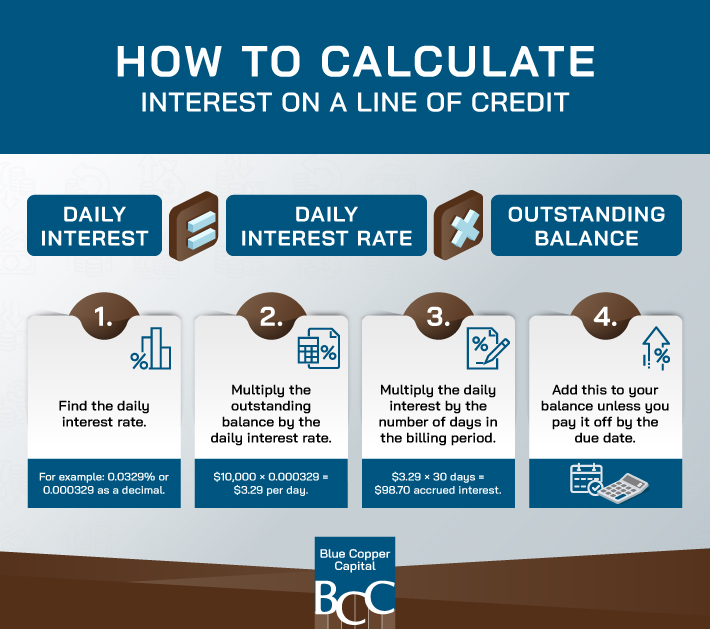

The interest is usually calculated daily by dividing your annual interest rate by 365 (or 360, depending on the lender’s policy) to get the daily interest rate. The daily rate is then multiplied by your outstanding balance, and the resulting amount is added to your current balance.

What Is a Line of Credit?

A line of credit is a revolving borrowing option that allows you to withdraw funds up to a set limit as needed, unlike a lump-sum loan. This flexibility makes it popular for covering unexpected expenses or managing cash flow. You only pay interest on the amount you use, not the overall credit limit.

Some examples of lines of credit include:

- Home equity line of credit (HELOC): Secured by your home’s equity, often used for home improvements or major expenses.

- Personal line of credit: Can be secured or unsecured and used for general purposes, such as emergency expenses.

- Business line of credit: Designed specifically for business cash flow needs.

The key advantage of a line of credit is that you maintain control over how much money you borrow and when you repay it. However, this flexibility comes with the responsibility of understanding how interest rates are calculated.

Understanding Interest Rates

The interest rate on a line of credit determines how much it costs to borrow money. This rate is typically expressed as an annual percentage rate (APR) but applied on a daily or monthly basis to calculate accrued interest.

Some key terms can help you navigate this process:

- Average interest rate: The typical rate that lenders offer for a particular type of credit, which varies based on factors such as credit score and loan type.

- Daily interest rate: The APR divided by the number of days in a year.

- Simple interest: Interest calculated only on the principal balance, which is the amount borrowed.

For example, if you have an APR of 12%, your daily interest rate would be 12% ÷ 365 = 0.0329% per day. This rate is applied to your outstanding balance to calculate the daily interest.

Factors Affecting Interest Rates

Several factors influence the interest rate you’ll be charged on a line of credit, including:

- Credit score: A higher credit score typically results in a lower interest rate.

- Loan type: Secured loans, such as a HELOC, have lower rates than unsecured loans.

- Market conditions: Economic factors, such as inflation and the Bank of Canada’s interest rate can affect rates.

- Line of credit usage: Consistently high usage or hitting your credit limit may lead to less favourable terms in the future.

Understanding these factors can help you negotiate a more favourable rate and manage your line of credit effectively.

Calculating Interest on a Line of Credit

Interest on a line of credit can be calculated either daily or monthly, depending on your lender’s practices. Here’s how both methods work:

Daily Interest Calculation

Daily interest is calculated based on your outstanding balance for each day. The formula looks like this:

Daily Interest = Daily Interest Rate × Outstanding Balance

For example, if you borrowed $10,000 with a daily interest rate of 0.0329%, your daily interest would be:

Daily Interest = $10,000 × 0.000329 = $3.29 per day

If this balance remains constant for 30 days, your accrued interest would be:

Accrued Interest = $3.29 × 30 days = $98.70

This is added to your principal balance unless it’s paid off by the due date.

Monthly Interest Calculation

Alternatively, some lenders calculate interest on a monthly basis. This involves applying the monthly interest rate to your average daily balance over the billing cycle.

Monthly Interest = (Average Daily Balance × Monthly Interest Rate)

The average daily balance method takes into account any fluctuations in your balance during the billing cycle. For example:

- Day 1–10 balance = $5,000

- Day 11–30 balance = $10,000

- Average Daily Balance = [(5,000×10) + (10,000×20)] ÷ 30 = $8,333.33

If the monthly interest rate is 1%, your interest for the month is:

$8,333.33 × 0.01 = $83.33

This method can benefit those who frequently pay down their balance during the billing cycle.

Strategies for Managing Interest on a Line of Credit

Managing interest effectively can help you save money and reduce financial stress. There are a few ways to do this, including making extra payments and refinancing.

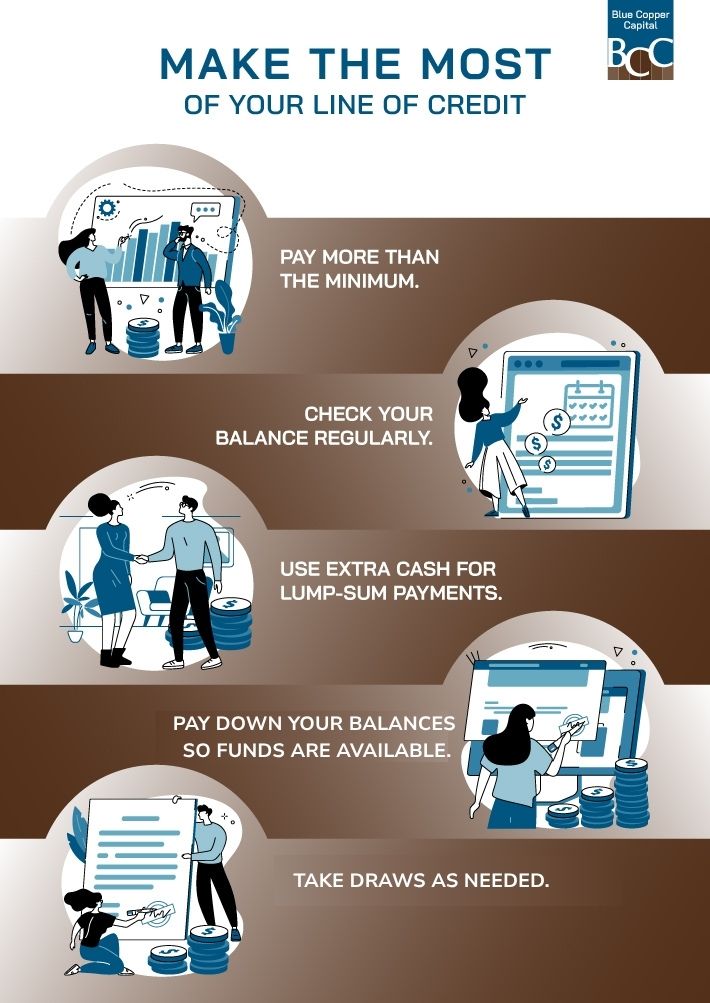

Pay More Than the Minimum

While it may be tempting to make only the minimum monthly payment, doing so keeps the principal balance high and increases the interest you’ll pay over time. Paying down as much as you can every month will reduce accrued interest and shorten your repayment period.

Monitor Your Outstanding Balance

Regularly check your balance and avoid borrowing more than you can comfortably repay. Many lenders offer tools to help track your balance and calculate potential interest costs.

Take Advantage of Lower Rates

If you qualify for a secured line of credit (e.g., a HELOC), you’ll benefit from a lower average interest rate compared to unsecured options.

Use Lump-Sum Payments

Whenever you receive extra income, such as a bonus or tax refund, consider applying it to your principal balance. This can significantly reduce the amount of interest you’ll pay over time.

Pay Down Your Balance so Funds are Available

Since a line of credit accrues interest daily or monthly, paying off your balance within 30 days can limit your interest expense. Use reminders to stay consistent and on-time with payments.

Take Draws As Needed

As long as your line of credit has available funds, you can access them when needed. Whether it’s for a visit to the dentist or a vacation in Denmark, you may use your credit to cover the costs.

Maximize the Benefits of Your Line of Credit

Understanding how interest is calculated on a line of credit allows you to make informed borrowing decisions. Whether you’re drawing from a home equity line of credit or managing a personal credit line, the key is to stay proactive about payments and budget for interest costs. By carefully managing your outstanding balance and taking advantage of strategies like making extra payments, you can minimize costs while enjoying the flexibility that a line of credit offers. If you’re unsure how to optimize your credit use, feel free to contact our team at Blue Copper Capital for advice. Explore our online resources to learn more about lines of credit and take control of your finances today. We’re here for you.