Credit card debt can feel overwhelming, especially when high interest charges make it hard to keep up with payments. Many Canadians face this challenge, with the average household carrying thousands of dollars in balances.

The good news is there are proven strategies to help you take control. From structured payoff methods like the debt snowball or debt avalanche, to balance transfers, and even personal loans that consolidate debt into one predictable payment, you have options to get back on track.

Before choosing a path forward, it’s important to understand how each strategy works, and which one best fits your financial situation.

Start With a Clear Budget

Before we dive into specific debt payoff strategies, you should understand exactly where your money goes each month. Creating a budget isn’t just about tracking expenses, it’s about finding extra money to put toward your debt. List all your income sources and expenses, including rent, groceries, streaming services, and coffee purchases.

Once you see the full picture, identify areas to cut back on spending. Even finding an extra $50 per month can speed up your payoff timeline.

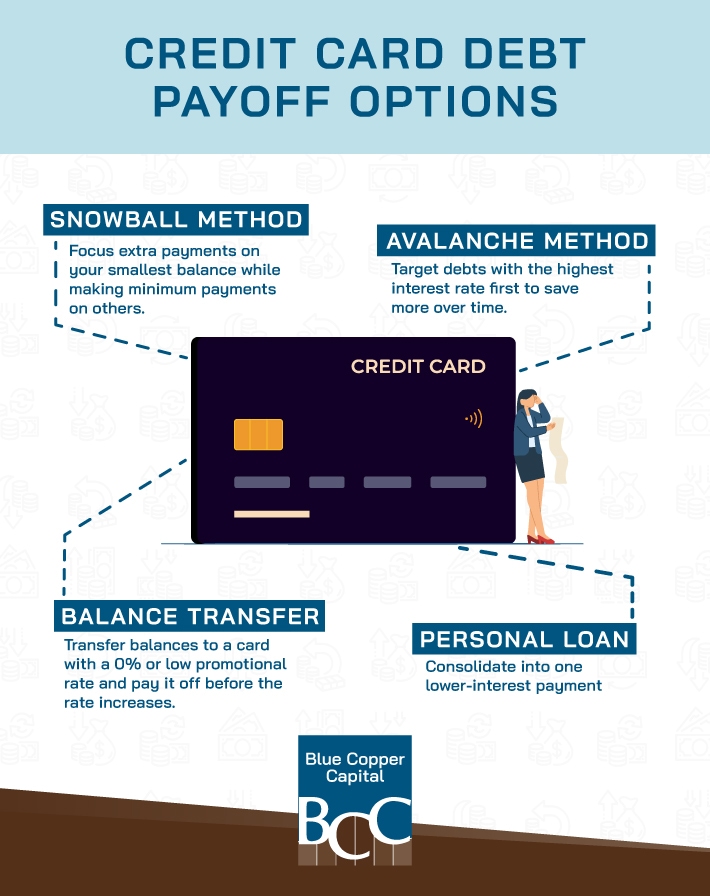

The Debt Snowball Method

The debt snowball method focuses on motivation and quick wins. With this approach, you’ll pay the minimum amount on all your credit cards, then put any extra money toward the card with the smallest balance.

Here’s how it works: once you pay off the smallest debt, you take that entire payment amount and apply it to the next smallest balance. This creates a “snowball effect” where your payments grow larger as you eliminate each debt.

The psychological benefits of this method are substantial. Seeing debts disappear quickly can provide the motivation you need to stick with your plan. However, you might pay more in interest overall since you’re not prioritizing high-interest debts first.

The Debt Avalanche Method

The debt avalanche method takes a mathematical approach to debt payoff strategies. Instead of focusing on balance amounts, you’ll target the credit card with the highest interest rate first while making minimum payments on everything else.

This strategy typically saves you the most money in interest charges over time. High-interest credit card debt can compound quickly, so eliminating these expensive debts first makes financial sense.

The challenge with the avalanche method is that it requires more patience. If your highest-interest card also has a large balance, it might take months to see that first debt disappear. However, the long-term savings can be substantial.

Debt Consolidation Through Balance Transfers

A balance transfer card lets you move multiple debts to one account, often with a promotional 0% or low interest rate. This means more of your payment goes toward the principal. These cards usually charge a transfer fee (2–5%) and require good credit to qualify. Since the promotional rate is temporary, you’ll need a plan to pay off the balance before it expires to avoid high interest charges.

Why Personal Loans Can Be a Smart Way to Pay Off Credit Card Debt

If you’re juggling multiple high-interest credit cards, a personal loan can be one of the most effective ways to take control of your repayment. By consolidating your balances into a single fixed-payment loan, you can often reduce interest costs, simplify your finances, and set a clear timeline to become debt-free.

- Lower interest rates: Personal loans often carry significantly lower rates than credit cards, which means more of your money goes toward paying down the balance instead of interest.

- Predictable payments: With a fixed repayment schedule, you’ll know exactly how much to pay each month and when you’ll be debt-free. This structure can make planning and budgeting easier.

- Debt consolidation: Instead of juggling several cards with different due dates and rates, a single personal loan consolidates everything into one payment.

- Credit rebuilding potential: Successfully paying off a personal loan on time can help rebuild your credit profile faster than struggling with revolving credit card debt.

Important considerations:

- A personal loan works best if you avoid taking on new credit card balances while you repay it. Otherwise, you could end up deeper in debt.

- Loan eligibility depends on your income, banking history, and identification — but lenders like Blue Copper Capital are often more flexible than traditional banks.

- Responsible borrowing is key. Only take out what you can comfortably afford to repay, and review all fees, interest rates, and terms before signing.

If you’re serious about tackling your credit card debt, a personal loan can give you structure, lower costs, and a clear path toward becoming debt-free.

Choosing the Right Lender for Your Situation

If you decide that a personal loan is right for your debt consolidation needs, keep these factors in mind:

- Look for transparency in rates, fees, and terms.

- Check for origination fees and understand their impact on your total loan cost.

- Find out if there’s a penalty for paying off the loan early.

- Review the repayment term length and how it affects both interest paid and monthly payment amounts.

- Assess whether the lender offers flexible solutions tailored to your financial situation.

- Consider how the lender supports borrowers beyond the initial loan process.

Loan Eligibility

To qualify for a personal loan for debt consolidation, you’ll typically need to meet certain requirements. Most lenders will expect you to:

- Have been employed for at least 90 days and be able to provide current and recent pay stubs.

- Maintain an active bank account, authorize pre-authorized debits, and provide the last 90 days of banking history in read-only form.

- Be at least 18 years old and a resident of the province where you’re applying, with valid government-issued identification (two pieces, one of which must include a photo).

- Request a loan amount that falls within the lender’s available range, which can vary depending on the institution and your credit profile.

Steps to Apply

Applying for a personal loan for debt consolidation is usually straightforward. The process generally includes:

- Choose your application method: Many lenders allow you to apply online, by phone, or in person at a branch location

- Complete the application form: Provide personal details, employment information, and the amount you wish to borrow

- Receive a decision: Some lenders can review your application and approve loans within the same day

- Review your loan offer: Carefully read the terms, interest rate, repayment schedule, and any applicable fees before accepting

- Finalize the paperwork and receive funds: Sign the agreement electronically or in person, then receive the loan amount via your chosen payment method

Tips for Responsible Borrowing

Responsible borrowing is about making decisions that support your long-term financial stability, not just solving an immediate problem.

- Borrow only what you can realistically afford to repay.

- Read the full terms of any loan agreement before signing.

- Review your debt-to-income ratio to ensure a new loan won’t overextend your finances.

- Make sure the monthly payment comfortably fits within your budget.

- If a loan would strain your finances, consider focusing on increasing income or reducing expenses instead.

- Treat a personal loan as a tool, not a quick fix.

- Address the spending habits that contributed to the debt in the first place.

Take Control of Your Credit Card Debt

Paying off credit card debt is possible with the right strategy — whether that’s budgeting, using the snowball or avalanche method, or consolidating balances. But if high-interest cards are holding you back, a personal loan can provide the structure and lower rates you need to make real progress.

At Blue Copper Capital, we specialize in flexible personal loans designed to help borrowers who may not qualify with traditional banks. Our team will work with you to find a repayment plan that fits your budget and supports your long-term financial goals.

Book an appointment today to explore your loan options and take the next step toward a debt-free future.